3. Prospectuses and takeover bids

The tasks of the FIN-FSA’s prospectus scrutiny team include scrutiny of prospectuses related to the offering and listing of securities as well as processing of interpretation issues related to prospectus regulations. Our takeover bid team, on the other hand, scrutinises offer documents related to public takeover bids, processes exemption matters and makes interpretations in issues related to takeover bids

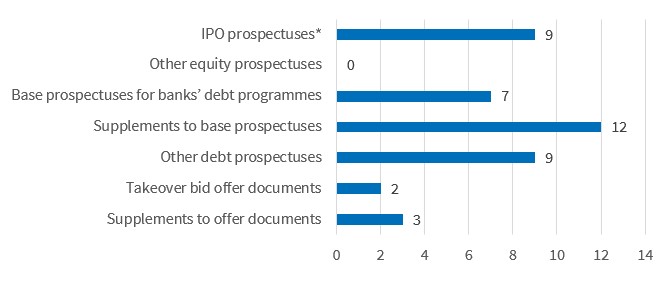

Prospectus and takeover bid cases in 2025

In 2025, the Financial Supervisory Authority approved 25 prospectuses and 12 prospectus supplements. There were a total of nine equity prospectuses and 16 debt prospectuses. All of the equity prospectuses related to listings. Of the debt prospectuses, seven were base prospectuses related to banks’ debt programmes. The remaining nine debt prospectuses were individual bond issuances, and four of them related to so-called green financing. By contrast, no prospectuses in line with the EU Green Bond Regulation, which became applicable from 21 December 2024, have been submitted to the FIN-FSA for approval to date.

With a prospectus approved in 2025, three completely new listed companies were listed on the regulated market, two companies transferred to the regulated market from the First North list, and two listings related to the demerger of a listed company. All of these companies published a full prospectus in accordance with Annexes 1 and 11, as required by the regulations. In addition, two companies prepared a prospectus approved by the FIN-FSA for the offering of shares and listed on the First North Growth Market. One of them used the EU Growth prospectus under Article 15 of the Prospectus Regulation, and the other prepared a full prospectus. All equity prospectuses were prepared in Finnish and, in addition, an English translation was prepared for seven prospectuses.

In 2025, we processed numerous interpretation issues related to, among other things, the emergence of the prospectus obligation and prospectus exemptions. Issues related to prospectus exemptions, in particular, increased after new prospectus exemptions became applicable from 4 December 2024. We also discussed with the drafters of prospectuses the financial information1 to be disclosed in listing prospectuses and the terminology2 to be used in listing arrangements, for example. We announced that we will discontinue providing advance comments3 on marketing material related to listing prospectuses . Last autumn, in connection with our scrutiny of listing prospectuses, we took a position only on marketing slogans and some specific issues.

On the takeover bid side, the FIN-FSA approved two offer documents and three related supplements, and granted one exemption from the obligation to launch a bid in connection with a published arrangement.

In 2025, interpretation issues related to takeover bids mainly related to acting in concert and equal treatment, particularly in consortium bids involving shareholders of the target company.

Figure 1 Number of prospectuses and offer documents in 2025

*The number of IPO prospectuses includes two list transfers and two demergers.

Source: Financial Supervisory Authority.

We provided a statement to the Ministry of Finance during the preparation phase of national regulatory changes related to the Listing Act. The FIN-FSA supported a proposal for a prospectus threshold of EUR 12 million in accordance with the Prospectus Regulation. Regarding the language of the prospectus, the FIN-FSA considered it important that when securities are offered to the public or listed on a regulated market exclusively in Finland, retail investors would continue to have the opportunity to read the prospectus in a national language. In addition, the FIN-FSA supported a proposed regulatory choice to continue to require a key information document in accordance with the Securities Markets Act in securities offerings that exceed one million euros but fall below the prospectus threshold. The FIN-FSA drew attention, however, to the fact that it might be appropriate to explore the need to update the content requirements of the key information document.

In 2025, we launched a thematic review of alternative performance indicators. The thematic review will assess how consistently issuers have presented the alternative performance measures contained in a listing prospectus in their financial reporting following the listing. In addition, the thematic review will assess how issuers have complied with ESMA Guidelines on Alternative Performance Measures. The thematic review covers seven companies that listed on the main list of the stock exchange in 2019–2022 and concerns the annual and half-yearly reports published by these companies in the first two years following the listing. The aim is to publish the thematic review in early 2026.

Prospectus scrutiny priorities in 2026

In prospectus matters, 2026 will be marked by significant changes to prospectus regulations. The content requirements for simplified types of prospectus (EU Follow-on prospectus and EU Growth issuance prospectus) will change on 5 March 2026, and the content requirements for other types of prospectus on 5 June 2026. We will focus on issues related to the changes in prospectus regulations, and participate in discussions of them at ESMA with other national supervisors.

In our prospectus scrutiny, we will continue to pay special attention to the comprehensibility of prospectuses, risk descriptions, information related to the adequacy of working capital in share prospectuses, and any sustainability information in debt prospectuses. We will also continue to develop and utilise a artificial intelligence tools to support prospectus scrutiny.

During 2026, we will add information and guidance related to changes in prospectus regulations to the FIN-FSA webpage “Offering of securities and prospectuses”. In addition, we will publish Market Newsletter articles on changes to prospectus regulations.

Prospectus scrutiny period and enhancing prospectus scrutiny

We will continue to try to scrutinise and approve prospectuses within 10 working days (IPO prospectuses within 20 working days).4 If necessary, however, we will exercise the option provided for in the Prospectus Regulation to calculate a new scrutiny period of 10 working days from the submission of a new draft prospectus. Prospectus drafters have the opportunity to influence the efficiency of prospectus scrutiny by preparing prospectuses carefully.

We express the hope that advisors or issuers will contact us in good time regarding plans for both debt and equity prospectuses, and particularly if the preparation of a prospectus under the European Green Bond Regulation is planned. It should also be noted that the Prospectus Regulation requires prior notification of five working days before an EU Follow-on prospectus is submitted for approval.

We will enhance prospectus scrutiny by moving more clearly to an operating model in which we only provide general comment on certain types of deficiencies that are repeated in several sections of a prospectus, instead of commenting on the issue in every relevant section of a prospectus. In addition, we ask prospectus drafters to confirm using the comment form that our comments have been taken into account throughout the prospectus. In practice, such a procedure may relate, for example, to the requirement to cite sources of information in a prospectus.

Observations on takeover bid cases

In 2026, we aim to continue to streamline the processing of interpretation issues related to the takeover bid regulations. These issues often concern entirely new types of situation that the FIN-FSA has not previously addressed. Advisors can influence the length of time it takes to process interpretation issues by providing a clear and comprehensive description of the arrangement and related issues, including the advisor’s own reasoned view. The length of time it takes to process interpretation issues is also affected by how much further clarification we need and the timeframe within which our questions will be answered. To ensure that our views are based on up-to-date information, advisors should pay attention to how we are informed about changes made to planned arrangements.

We will continue to participate in the activities of ESMA’s working group on takeover bids. The group discusses, for example, regulatory interpretations related to takeover bid regulations.

Through a 2024 amendment to the Security Markets Act, takeover bid and flagging regulations were extended to be applicable to a multilateral trading facility (First North companies) in addition to a regulated market. In the same context, the FIN-FSA was given the authority to issue provisions on grounds by which persons are not deemed to be acting in concert. The FIN-FSA has, among other things, started updating the FIN-FSA Regulations and guidelines (9/2013) on this issue.

1 Market Newsletter 3/2025 Inclusion of long financial time series in an equity prospectus

2 Market Newsletter 3/2025 Guidance on terms related to listings

4 The scrutiny period for an EU Follow-on prospectus is seven working days in certain situations.