Audit committees and auditing

The Financial Supervisory Authority (FIN-FSA) acts as the competent authority, in accordance with Article 20(2) of the EU Audit Regulation, in monitoring and assessing the performance of audit committees, as referred to in Article 27(1)(c) of the Regulation. (Act on the Financial Supervisory Authority, section 50i)

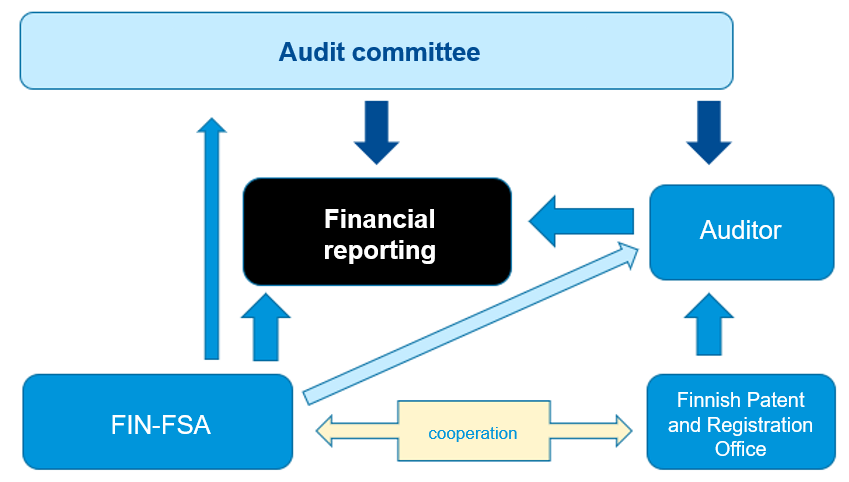

The Auditor Oversight Unit and the FIN-FSA cooperate as appropriate with regard to auditor oversight and audit committee issues. (Auditing Act, chapter 9 section 2)

When required for the oversight of a supervised entity referred to in sections 4 and 5 of the act on the Financial Supervisory Authority (878/2008) or another financial market actor, the FIN-FSA may investigate if an auditor has acted in compliance with this Act and the statutes issued by virtue of it, or the provisions of the EU Audit Regulation applicable to the entities in question. The FIN-FSA may present a supervisory matter for the Audit Board to decide. (Auditing Act, chapter 9 section 2)

The FIN-FSA may, for a maximum of three years, prohibit a person from acting as member of an administrative body or as managing director of a public interest entity, as referred to in chapter 1 section 9 of the Accounting Act, if the person has as a member of an administrative body or as managing director seriously violated or breached the maximum duration of engagements stated in chapter 5 section 1 of the Auditing Act and the preparation of the appointment of an auditor, and the provisions of sections 3 and 4 related to non-audit services or the provisions of Articles 16 and 17 of Regulation (EU) No 537/2014 of the European Parliament and of the Council on specific requirements regarding statutory audit of public-interest entities and repealing Commission Decision 2005/909/EC, hereinafter the EU Audit Regulation, on the appointment of statutory auditors and audit firms and the duration of an audit engagement. (Act on the Financial Supervisory Authority, section 28a)

FIN-FSA actions with regard to audit committees:

- Audit Committee survey of the implementation of sustainability reporting

- Report on the Audit Committee Survey 2020, in cooperation with the Finnish Patent and Registration Office (news release, report)

- Audit Committee Event 2019, in cooperation with the Finnish Patent and Registration Office (presentation material)

- Letters in connection with full review of financial statements (What does IFRS enforcement mean for listed companies? (in Finnish) – video script in English)

- Questionnaire to audit committees on the adoption of new IFRS standard on sales revenue in 2016 (Letter 1, Letter 2, presentation at listed companies event 2016 (all in Finnish))

See also

Event for listed companies 2022: Results of CEAOB audit committee surveys (in Finnish)

Market newsletter 2/2021: Role and practices of audit committees subject to European Commission

IFRS enforcement and e.g. Listed companies event 2020 (in Finnish) (Significance of audit committees and auditing challenges)

Finnish Patent and Registration Office Auditor Oversight and e.g. Annual Quality Inspections Report 2020 (in Finnish)

CEAOB and e.g.

- Market Monitoring Questionnaire to Audit Committees in Finland (2022)

- Report on the CEAOB survey - Materiality in the context of an audit – July 2022

- CEAOB Analysis on Audit Committee indicators collected as part of the 2nd Market Monitoring report (2020)

European Commission reports 2021 and 2017 on developments in the EU market for statutory audit services to public-interest entities pursuant to Article 27 of Regulation (EU) No 537/2014.

IOSCO and e.g. IOSCO Report on Good Practices for Audit Committees in Supporting Audit Quality (2019)