9. Audit committees are involved in sustainability reporting implementation projects

The main implications of the government’s proposal state that the implementation of procedures in line with the new sustainability reporting requirements will be a challenging effort for each company. According to the proposed amendment to the Accounting Act, the sustainability report must include a description of the tasks of the board of directors and the chief executive officer in relation to sustainability matters.1

The FIN-FSA asked audit committees to describe their company’s process or plans to implement sustainability reporting, and the role of the board of directors, the audit committee and the chief executive officer therein (question 4).

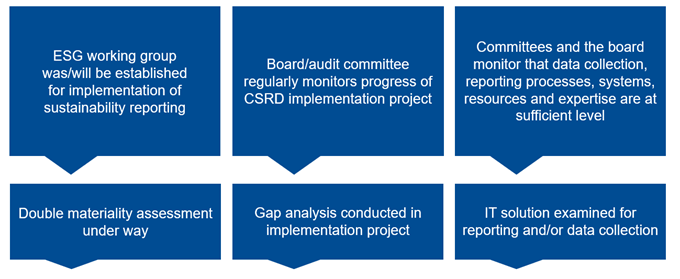

Figure 9. Examples of responses to question 4

Based on the responses, the measures required by companies to implement the new sustainability reporting are under way or are planned to be launched in the near future. Companies have organised themselves, defined the necessary roles and allocated responsibilities, taking into account the company’s sector and size. A number of companies have set up a cross-functional project team for the implementation of the new regulations, while others have established a dedicated unit for reporting and measures on sustainability matters. One respondent stated that “the Group Corporate Responsibility Team leads several ESRS-related projects and operations in 2023–2024 and it reports progress to the Group Executive Team and the Board of Directors”.

Around half of the audit committees responded that a double materiality assessment and/or gap analysis has been carried out, is in progress or is planned. An example answer states: “In spring and summer 2023, the company carried out a double materiality assessment based on previous materiality assessments and, in collaboration with a consulting firm, the company launched a gap analysis to clarify the difference between the content of the current corporate responsibility report and the requirements of the ESRS. The gap analysis was completed during the summer and subsequently supplemented once the final ESRS standards were available. During autumn 2023, the exact data sources and reporting systems will be identified and the annual reporting process will be developed.”

The role of the CEO was described, among other things, as follows: “directs the work of the sustainability team”, “is responsible for ensuring that the company’s sustainability reporting is reliably organised and implemented in accordance with the regulations and strategy”, “ensures that sustainability reporting is implemented and is sufficiently prioritised in the company’s management” and “ensures that resources and expertise are adequate to implement CSRD reporting, and that reporting and related processes and metrics support the company’s sustainability work”.

The responses revealed that the audit committee, among other things, “discusses management’s plan for the practical implementation of CSRD reporting”, “monitors the progress of implementation at all of its meetings”, “discusses the determination of double materiality”, “discusses the results of the gap analysis”, “assesses sustainability risks”, “is responsible for the implementation, processes and oversight of reporting”, “reports key findings on the progress of the project to the board of directors” and “supports the board of directors in sustainability reporting and the preparation thereof”.

Based on the responses, the board of directors, among other things, “is responsible for the sustainability strategy”, “defines sustainability reporting goals and responsibilities”, “monitors the progress of implementation”, “is responsible for ensuring that reporting is implemented in accordance with the CSRD”, “approves the determination of double materiality” and “monitors and evaluates reporting and assurance with regard to sustainability matters, in particular the reporting system, the effectiveness of internal control and auditing and of risk management systems, and the independence of the auditor”.

According to the understanding obtained by the FIN-FSA, sustainability reporting implementation projects have been launched or implementation plans are well advanced. There are different company-specific options in organising implementation, but the FIN-FSA believes that companies should have a dedicated project for the implementation of sustainability reporting, the progress of which would be closely monitored by the audit committee. On the other hand, the FIN-FSA considers the implementation schedules for companies that only started in autumn 2023 to be challenging. Effective audit committees have clearly defined procedures.

1 Government proposal 20/2023 vp, p. 17 (Proposals and their implications) and Act on the Amendment the Accounting Act, chapter 7, section 6. (in Finnish).