4. How was the survey conducted?

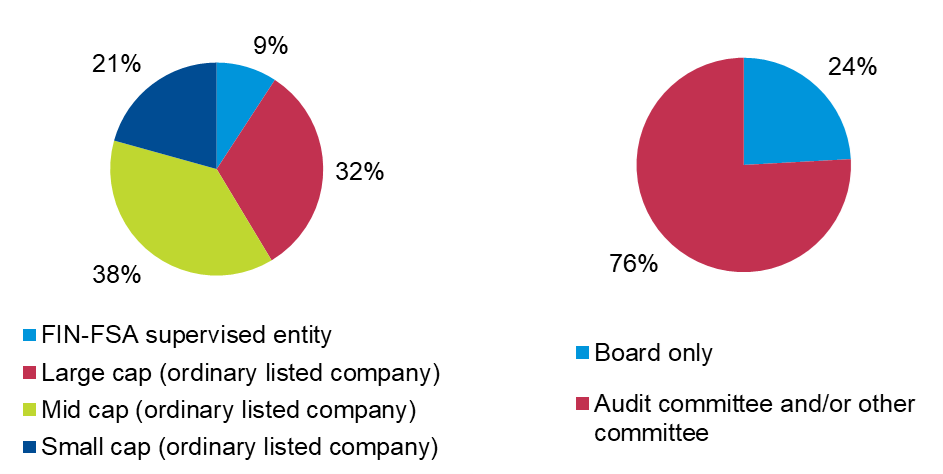

The FIN-FSA survey was sent to 92 entities (“companies”) that will prepare the sustainability report required by the CSRD as part of their 2024 management report. A total of 87 audit committees or boards of directors responded to the survey. Eight responses were received from FIN-FSA supervised entities (credit institutions and insurance companies) (Figure 2). The responses were for the most part commendably thorough.

Figure 2. Companies represented by the respondents (N=87) |

Figure 3. Whose responsibility is it to prepare corporate responsibility or sustainability reporting? (N=87) |

Source: Financial Supervisory Authority

In the survey and in this report, the term audit committee refers to an audit committee, another committee carrying out the tasks of an audit committee, or the full board of directors carrying out the tasks of an audit committee.

The preparation of corporate responsibility or sustainability reporting is part of the audit committee’s or other committee’s tasks in around three quarters of the companies (Figure 3). In seven companies, preparation is the task of another committee in addition to an audit committee. In two companies, the preparation is solely the task of a committee other than an audit committee. In two companies, corporate responsibility or sustainability reporting is solely the task of the board of directors, even though the company has, for example, an audit committee. The responses revealed that in addition to the audit committee or other committee, the board of directors also has a role in preparing corporate responsibility or sustainability reporting. The responses also revealed that not all companies have yet decided on the division of responsibilities. It was stated, for example, that “an official decision on which committee will monitor sustainability in the future has not yet been made at the time of writing this response”.

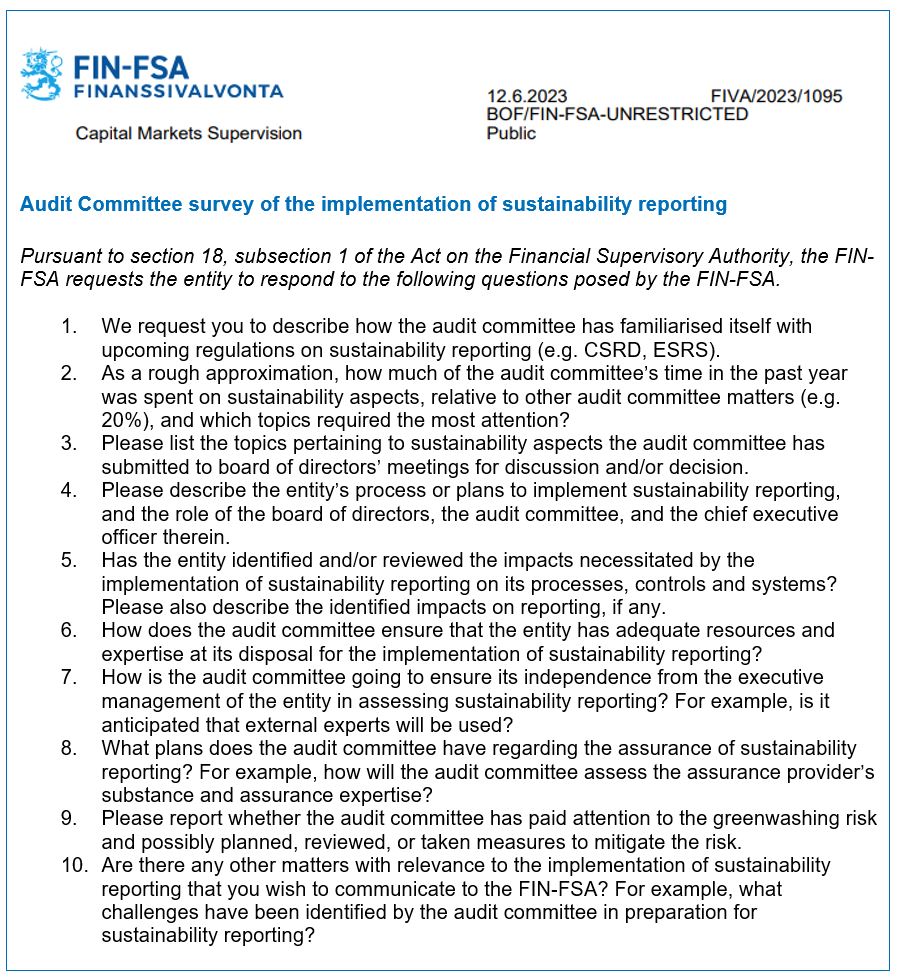

The questions asked by the FIN-FSA were, with the exception of background questions, open questions with no answer options. The objective of the open questions was to obtain company-specific, qualitative information on preparations for the sustainability reporting. The responses are therefore not fully comparable, and no unambiguous conclusions can be drawn from them, but the results should be considered as indicative. The responses are analysed in chapters 6–15.

In the report, the FIN-FSA quotes from the responses it received. The quotations given represent mainly, the response of more than one audit committee. The use of quotations is considered to give the reader a concrete overview of the responses received by the FIN-FSA.

Figure 4. The FIN-FSA’s questions1 to audit committees regarding the implementation of sustainability reporting

1 The letter can be read in full on the FIN-FSA website.