State of financial markets

In 2025, the operating environment of the Finnish financial sector was characterised by rapid changes in international geopolitics and trade policy as well as weak domestic economic development. However, strong capital adequacy shielded the financial sector from the high risks in the operating environment.

Finland’s anticipated economic upturn failed to materialise. The economy did, however, rise from recession in the final quarter of 2025, and gross domestic product grew by 0.2% for the year as a whole. The subdued economic situation led to higher unemployment and bankruptcies, while consumer confidence was put to the test. In addition, the situation in the housing market, the construction sector and the real estate market remained weak, elevating credit, investment and liquidity risks for the financial sector.

Interest rates were nevertheless lower in 2025 than in 2024, supporting borrowers’ debt-servicing capacity. Trading volumes in existing homes and in professional real estate transactions also increased, exports grew and business confidence improved towards the end of the year. According to the Bank of Finland’s economic forecast, economic growth will accelerate this year and strengthen further in 2027.1

Equity indices rose sharply especially in the United States, supporting, among other things, the investment returns of pension and insurance companies. Geopolitical and trade-policy developments rattled the markets, however, and there were at times large fluctuations in equity indices.

Despite the recovery in confidence and the improved economic outlook, general uncertainty is keeping risks elevated in the Finnish financial sector. Downside risks include the continuation of geopolitical and trade-policy tensions, weaker-than-forecast economic development in Finland, a deterioration in the employment situation, a continued decline in real estate prices and a drying-up of trading. Should these risks materialise, combined with the financial sector’s vulnerabilities, they could trigger a negative trajectory. In addition, the increase in hybrid and cyber attacks further underscores the importance of preparedness for operational risks and their management.

In addition to short-term risks, the financial sector’s operating environment is affected by longer-term structural trends such as climate change, demographic change, digitalisation, new technologies as well as new types of products and business models (e.g. cloud services and artificial intelligence). These trends alter the operating practices, competitive landscape and cost structure in the financial sector, and may also create new earnings opportunities. At the same time, they may also introduce new kinds of risks, the controlling of which will necessitate the development of risk management in the financial sector.

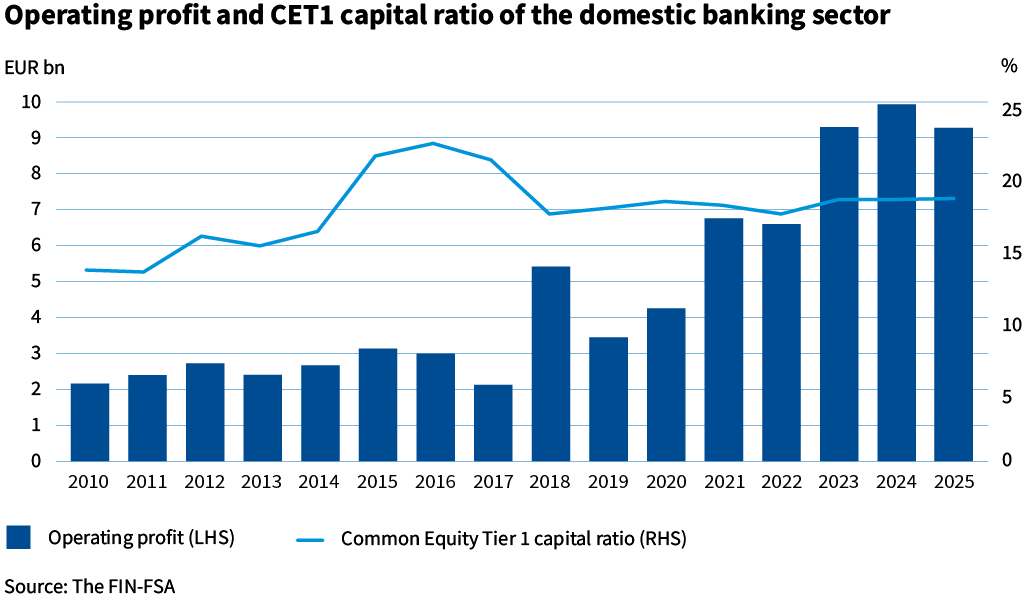

Profitability of banking sector weakened by lower net interest income, but capital adequacy remained strong

The banking sector’s capital adequacy remained strong in the review year. As a result of changes in European capital adequacy regulation that entered into force at the beginning of the year, the banking sector’s risk-weighted assets increased, which was reflected in a slight weakening in capital adequacy ratios and a reduction in own funds. On the other hand, the accumulation of retained earnings and issuances of capital instruments eligible as own funds increased the amount of own funds during the review year. Banks continued to hold ample capital relative to requirements. Capital ratios remained above the European average.

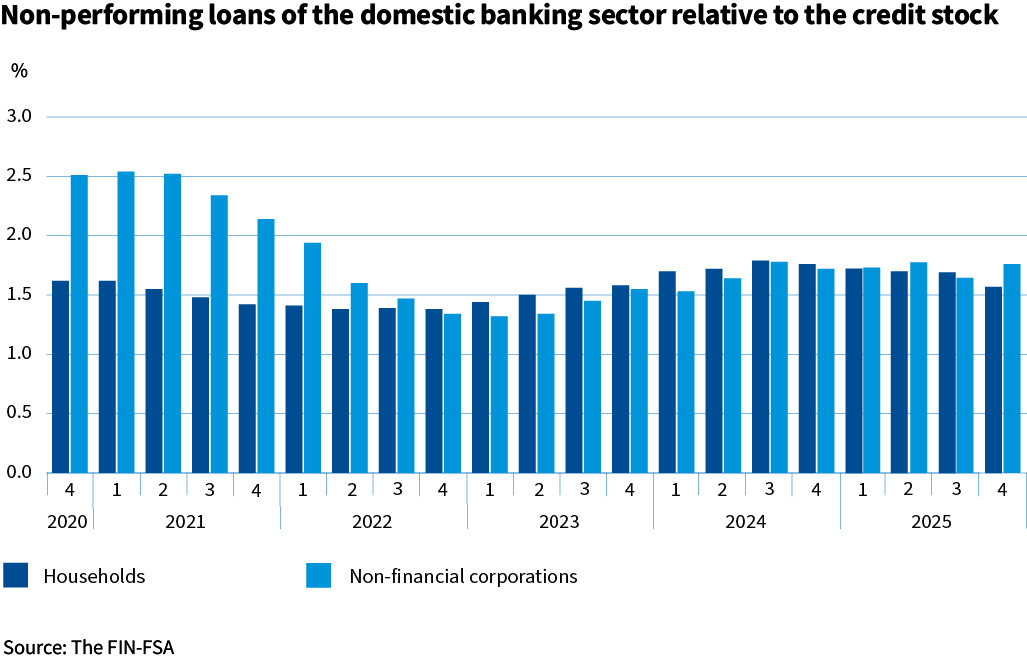

The banking sector’s operating profit declined, driven by lower net interest income than in the comparison year. Net interest income remained the most significant source of income for Finnish banks. The decline in net interest income nevertheless slowed towards the end of the year. Moreover, positive developments in impairment losses offset the reduction in earnings caused by the lower net interest income. The banking sector’s non-performing loans remained at a low level, among the lowest in Europe. The share of non-performing household loans declined slightly during the reporting year. The share of non-performing corporate loans, by contrast, was slightly higher than a year earlier. Towards the end of the reporting year, on the other hand, modest signs of improving credit quality were seen in certain corporate loan segments, such as construction. However, bank-specific differences in credit-risk developments were large.

The banking sector’s liquidity position remained strong. The cost of market funding remained stable during the review year. At the same time, the average interest costs on deposits continued to fall. Diversified funding sources and banks’ strong capital adequacy improve the availability and terms of market funding, while providing safety against financial market disruptions.

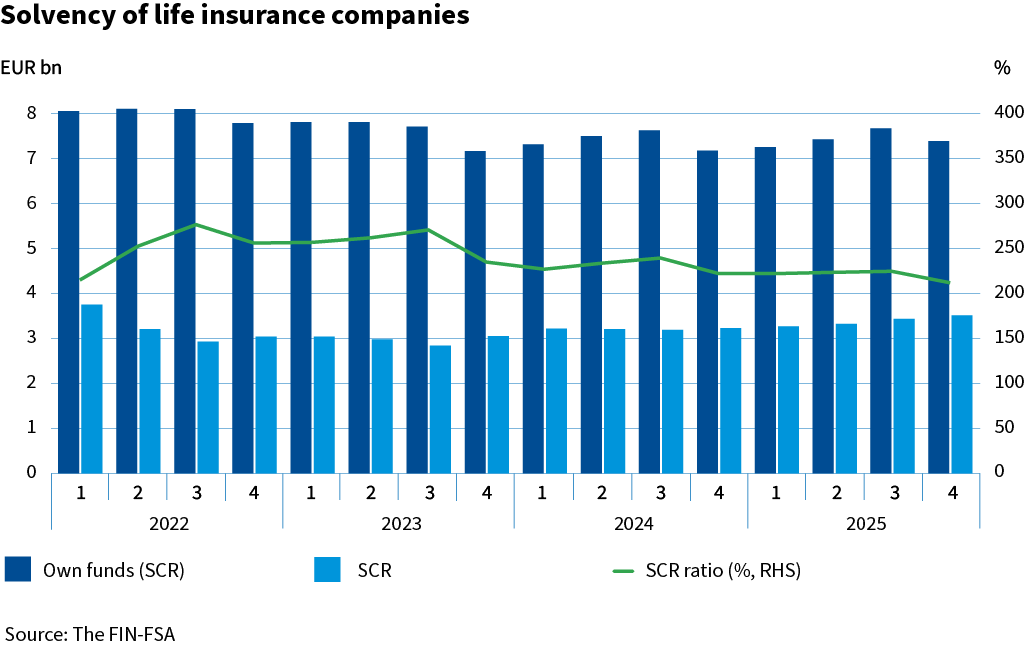

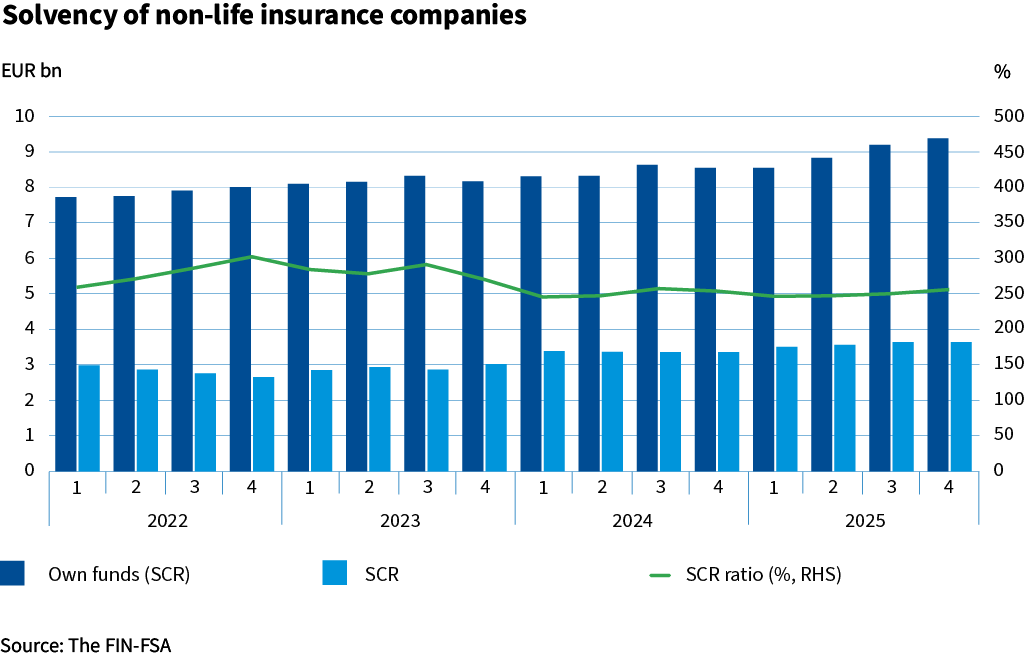

Life and non-life insurance companies’ solvency remained strong with no major changes

The solvency ratio of the life insurance sector declined during 2025 to 212.1% (12/2024: 222.4%), as the Solvency Capital Requirement (SCR) grew faster than own funds.

Life-insurance companies’ investment returns for the review year were positive (2.8%). Returns on fixed-income, equity and other investments were positive. Equity investments performed best (10.6%). Real estate investment returns remained slightly negative. Premium income grew from the previous year, particularly owing to growth in sales of savings life insurance and capital redemption policies. Claims paid increased slightly from the previous year.

At the end of the review year, the non-life insurance sector’s solvency ratio was at a good level at 256.5% and slightly higher than in the previous year (12/2024: 254.4%). Own funds grew slightly faster than the solvency capital requirement.

The investment returns of the non-life insurance sector were 4.5% in the review year. Returns on equity investments were 9.6%, while returns on fixed income and real estate investments were clearly lower but still positive. Non-life insurance premium income grew slightly from the previous year. Growth came particularly from sickness and motor vehicle insurance. Claims expenses were close to the previous year’s level.

The sector’s claims ratio was slightly better than in the previous year and the insurance technical margin was higher, but overall sector profitability declined year-on-year in the review year owing to lower investment returns.

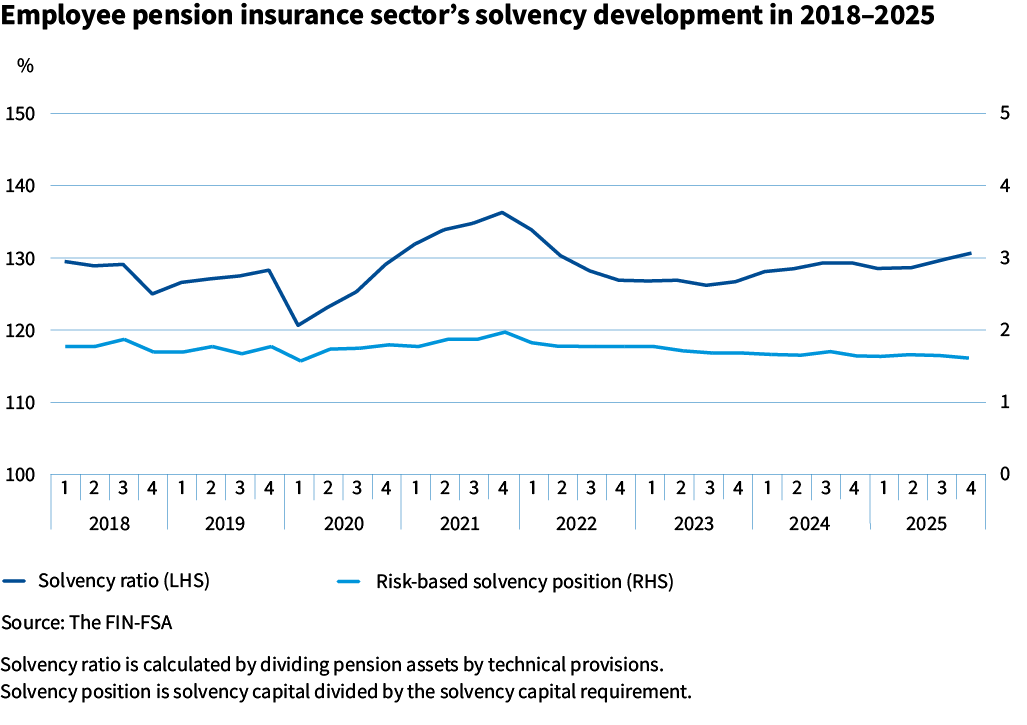

Solvency ratio of the employee pension sector strengthened owing to positive investment returns

The solvency capital of the employee pension sector grew during the review year owing to positive investment returns (7.7%). The solvency ratio, which indicates the ratio of solvency capital to insurance liabilities, strengthened during the year as solvency capital grew faster than insurance liabilities.

The solvency position, which refers to solvency capital divided by the solvency limit, remained at the previous year’s level (1.6), as the solvency capital increased at the same pace as the solvency limit. The solvency limit was raised by the growth in investment assets and the higher equity allocation.

All asset classes had a positive return in the review year. Equity investments performed best, and their share of the investment allocation rose to 56.3%. Employee pension institutions’ resilience to equity shocks remained broadly unchanged from the previous year, at a reasonable level.

Fund management companies and investment service providers’ result close to the previous year’s level

During the review year, the domestic fund sector’s assets grew to a record level, exceeding EUR 220 billion. Although fund assets declined in the spring owing to the US tariff war, they recovered quickly from the dip. Growth in the fund sector’s assets concentrated in UCITS funds, which account for nearly 80% of the entire domestic fund sector. The situation in open-ended real estate funds remained difficult in the review year, although some deferred redemptions were executed.

The historically high fund assets were also reflected in the results of fund management companies and investment service providers, which improved in the second half of the year after a weak start. The positive earnings trend was particularly visible in fund management companies, whose third- and fourth-quarter results were exceptionally strong. For fund management companies, the largest income and expense items continue to be fee income and expenses, which offset each other. For investment service providers, most of the income comes from asset management, and assets under their management have grown steadily. On the other hand, investment service providers’ costs have increased each year, putting pressure on earnings development.

FIN-FSA-related topics most visible in the media

1. Russia sanctions

2. Cybersecurity and scams

3. Real estate fund closures

4. Decisions of the FIN-FSA

5. Investigations related to Oma Savings Bank

1 Further information on the state of the Finnish economy in the Bank of Finland's economic review and forecast: Suomen talous kulkee vaakatasossa – Euro ja talous (in Finnish) and Finland’s economy heading out of recession – Bank of Finland Bulletin.